Happy 4th of July!

I’ve decided to go back to making semi-monthly payments. Waiting an entire month to see my balance drop was feeling excruciatingly slow. I think this way will keep me more motivated.

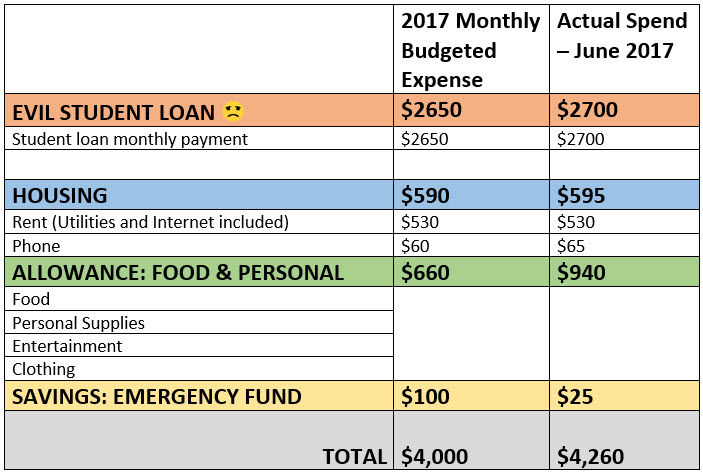

Expenses are going up

Fireworks aren’t the only thing going up these days. I have higher expenses. Two years ago, my enjoyment of Independence Day was clouded by a rent increase, initially of a lot, although later it ended up being less. Well, I got the news that my rent is going up again, so I will now pay $550 per month for my little room. My roommates’ rents are increasing by the same amount as well for their rooms. I’m still not complaining as my rent remains below market rate.

In my last post, I challenged the rising interest rates to come at me, and now they are. Just got a notice that my interest rate will be going up by an additional 0.20% starting this month. Whatever. I’m not stressing out. Interest may have speed, but I have endurance.

My spending is going up

The biggest money pit in my budget has been food. I know I’ve been overspending for a while, but I was afraid to look.

I don’t have transportation listed here because my monthly public transit pass is paid for from my pre-tax income.

Look at that $940!!! Ugh!

Where did I get the $260 to cover the overspend? My Opportunity Fund. Sigh. It’s taken a beating so far this year. On my To Do list is finding a way to spend less on food.

Financial Independence Day

My hopes are going up. With my balance dropping, this time of year is also inspiring me to think about my own financial independence day, which is currently November 15, 2019. That’s the day I’ll make my last student loan payment. After that? Freedom!!!! And some seriously bad dancing!

“Debtor’s prison is real, and opportunity cost is a bitch.” (DDSW)

(List of links to all DDSW posts)

You are chugging along well. Yup, gotta get that food and allowance category down, though! It would be nice to see your opportunity fund increase more so that you could work in something fun.

LikeLike

Yeah, this will be a challenge. I need to keep my spending in check so I can preserve that opportunity fund for travel to see family later this year.

LikeLike

I’ve been having some food spending issues as well, lately. I think the root of the issue is that I stopped using cash for all my food — it makes it so easy to just swipe an extra meal or add some fancy cheese to my grocery cart! Returning to cash this month.

The other thing I do when I need to get my food budget under control is think realistically. I know that there are circumstances in which willpower is absolutely not going to keep me from spending unnecessarily: if I’m out somewhere and I’m really hungry, I’m definitely buying a scone or whatever. So I try to keep some trail mix or an apple in my purse. Similarly, I think about foods I like to eat at home, and instead of trying to switch completely, I try to just not buy the three most expensive things on the list, and instead eat more of the cheaper things. Peanut butter instead of almond butter, that type of thing. For me it’s *all* about pre-planning because in the moment, I don’t usually have the mental wherewithal to make the right decision.

LikeLiked by 1 person

Very true about the card swiping. And yeah, failing to plan is planning to fail. I also have the added difficulty of having to try to work around numerous food intolerances, allergies and other health issues that require a more restrictive diet. The types of things that I used to cook/prepare in college are things that I can’t eat anymore. Ugh! Well I didn’t go to school for nothin’. I’ll put my fancy book learnin’ to work and come up with a plan.

LikeLike

That’s only two years till you’re debt free! So exciting. Your discipline is inspiring 🙂 🙂

LikeLike

Thank you! Seems light years away though, sometimes. 🙂

LikeLike

Food can definitely whack your finances. It’s so frustrating. I still think you are on a great path and a good pace.

LikeLike

Agreed!

It’s too bad about the rent increasing, but it’s a big plus it’s still below market rate. The interest rising is annoying. Grrrr. But seems like you’re doing great anyway and at least it’s better than it used to be. Are you willing to share how much more it will cost you per month?

Hang in there!

LikeLiked by 1 person

I’m not sure. I’d guess, an additional $5-$12/mo? The total interest per month will decline as my balance drops.

LikeLike

Thanks, ZJ.

LikeLike

To cut money on food, definitely cut out meat, if you eat it. it helps a lot. And I started googling blog posts about people who live on $100 for groceries for the month, to try to get ideas. Does that $940 include eating out? Because you and I both know that’s the biggest budget buster. When I’ve been tempted to stop at Subway or something on my way home from work, I then ask myself “would you rather spend this money now and have to work that much harder to earn it somehow else and then pay off your debt, or do you think you can handle waiting the few extra mins it’s going to take to get home?” That usually helps me put it in perspective. That, and I would have to write it in my Mindful Budgeting planner and keep on looking at the expense, which would probably piss me off, quite honestly.

I LOVE how you refer to it as the evil student loan in your worksheet. Damn straight they are pure evil!

LikeLike

Yes, it does involve lots of takeout and even, GASP!, some delivery!!! I know. I know. I’ve gotten so lazy and used to convenience. Yeah, need to work on a plan. Thanks, Terri. That’s a good way to think about it.

LikeLike

Food is sneaky. In the (30 day long) month of June, my budget (for myself and my generally modest in appetite kid), the spending amounted to just over $700. It includes 3 trips to restaurants (Cheesecake Factory type), as parents were in town the last couple of weeks, and I couldn’t let them pay for all outings in clear conscience.

Would it help if you ‘roboticized’ your diet to the point where every Monday you eat the same thing (down to the flavor of a granola bar and 3 peanuts/grapes level of precision), every Tuesday the same thing, every Wednesday the same thing, etc…. and then maybe on Sundays you go free style and ‘reward’ yourself with what you are in the mood for (within reason budget and portion size wise)? I know it works great for me, as long as the ‘design’ is good, done in advance to account for obtaining/consumption logistics, prep time, packing time, nutrition balance, and – of course – the budget. I can send you some sample menus that I utilize if you’d like. Surely, our food preferences and cooking schedules may be out of sync. But let me know.

Happy belated Independence Day – the day off of work for all of the free, and none of the hustlers. Oh well… 😛

LikeLike

Hmmm. That’s something to look into. It would cut down on the decision fatigue of dealing with meal prep everyday.

I’ll add this to my list of things to consider. Thanks! 🙂

LikeLike

As a person who has also refinanced her student loans, I suggest you start looking into that 5% fixed rate you mentioned once your variable rate hits 4.5% (if not sooner since interest rates are continuing to rise). That will give you time to complete the paperwork and transfers before your variable rate gets greater than the 5% fixed rate. Once you go over 5% in the variable, it will be more difficult to refinance to a fixed rate that is lower than that. It’s like what happened to your credit card rate, why would a student loan servicer give up that kind of money? Refinance to the great fixed rate while you can!

LikeLike

Hi Sara! Yeah. I’m keeping an eye on the rate. I’m planning to try another refinance later this year.

LikeLike