Happy New Year!

It is that time of year again. I unveil my 2015 financial goals. Before I do, I’ll look back at my recent yearly goals.

2014 Goals:

- Pay off remaining $22,770 balance in credit card debt

- Open and contribute to 401k up to point of employer match when eligible

2014 Outcome: [partial success]

- Paid off $16,780 in credit card debt [remaining balance: -$5,990]

- Paid $8,720 in student loan interest [0.o -Yeah, this is insane.]

- Opened and contributed to retirement funds [+$6,578 (including employer match)]

In the footer and sidebar, I have added a tracker for my retirement and other savings to help me have a fuller picture of my finances.

2015 Goals:

- Pay off remaining credit card debt of $5,990

- Reach $20,000 in retirement savings

- Reduce student loan debt to $108,000

- Save $6,000 in savings (Yes, my lack of an emergency fund is scary.)

- Pay cash for an international trip – $??

My student loan goal doesn’t look like much of a drop, but you have to remember that the first $750 that I pay each month is just going to interest, not principal. So it will take nearly $15k in payments to get from $113k to $108k.

Undoubtedly, I have some more thinking to do to figure out how to prioritize all of these goals. Save for retirement or pay down debt?

Will a noble samurai rescue me from my quandry? Enter FS-DAIR

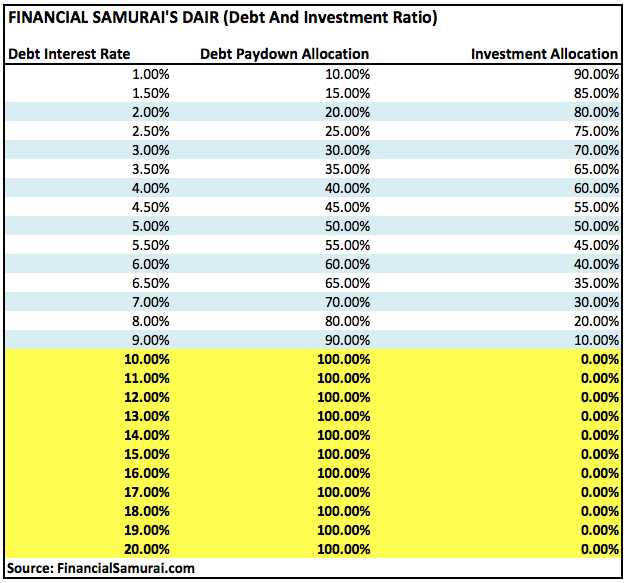

Financial Samurai has posted a formula for determining how to prioritize debt repayment vs. retirement funding. His FS-DAIR (Financial Samurai Debt and Investment Ratio), looks like the tool I’ve been hoping to find for a while now. How does it work? This chart lays it all out in a clear format.

Source and Image Credit: FinancialSamurai.com

Source and Image Credit: FinancialSamurai.com

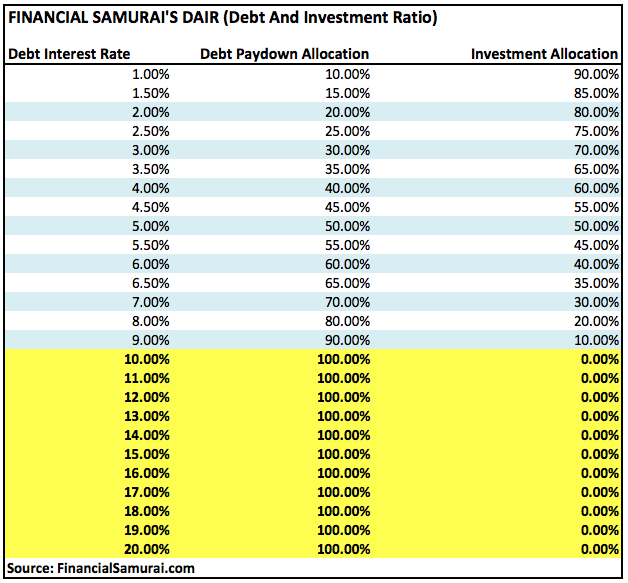

Basically, any debt that you have carrying 10% or higher in interest, should be paid off post-haste, at the expense of any investing (beyond the 401k employer match). Once your debts have interest rates at 9% and below, things get interesting. Read Sam’s FS-DAIR post for examples of how this works. For instance, Sam uses the following as an example for someone deciding how much to put toward student loans vs 401k.

Source: FinancialSamurai.com

Source: FinancialSamurai.com

My student loan debt is made up of many separate loans with different fixed interest rates. I will need to run the numbers to see how this would shape my plan of attack. I’ll do a follow-up post on this in the not too distant future. Thanks, Sam for lending me a sword to use in my battle!

Net Worth – Double Debt Single Woman – January 2015

As my debt drops in 2015, I’ll be tracking my Net Worth. My first goal will be to see it drop down into the 5-digit zone. Soon you will also be able to track it here @Rockstar Finance. I will be pretty low on the ranked list, but I will be gunning for higher and higher slots. Watch out Finance Phoenix and Feisty Finance!

“Debtor’s prison is real, and opportunity cost is a bitch.” (DDSW)