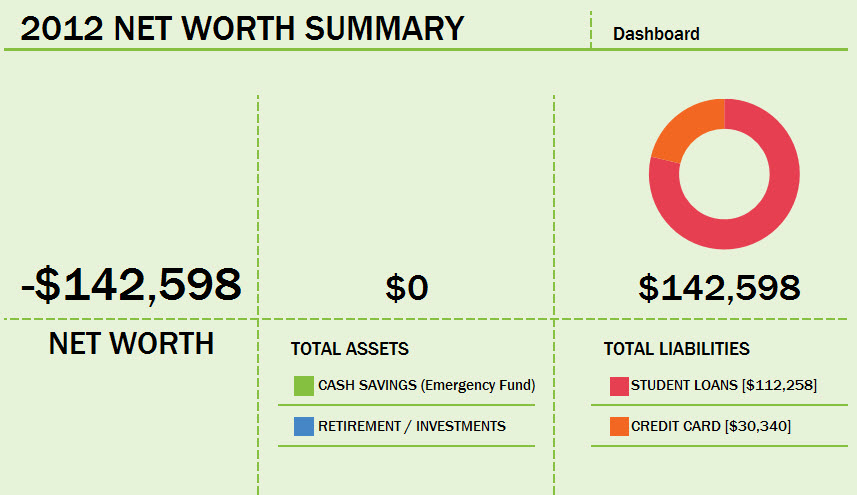

Double Debt Single Woman Has Paid Off Over $142,598 and is Officially Debt-Free!

I took this image from my footer at the bottom of this page. This is so beautiful, I had to frame it!

IIIIIIII’MMMM DDDEEBBBTTT FFFFRRRREEEEEEEEEEEEEE!!!!!!!!!!!!!!

I had to include my own Dave Ramsey style debt-free scream!

I’ve paid off over $142,598 of debt ($30,340 of credit card and $112,258 of student loan). This number represents principal debt only. When I estimate the interest payments, and the medical debt I’ve also incurred and paid off over the years since starting this blog, I’ve easily made over $170,000 in actual total debt payments. Sigh.

But you know what? It makes the celebration that it’s finished, all the better. Read More