Debt Update: February 2015

Hey Peeps!

I know. I know. Long time, no write.

Where have I been? Where else… at work. I certainly can’t afford to go anywhere else. I had a string of projects that left me too drained to blog. It all culminated in an all-nighter session to get some deliverables submitted on time that took me three days to recover from. Getting older sucks.

Since then, things at work have returned to a manageable level…at least for the time being.

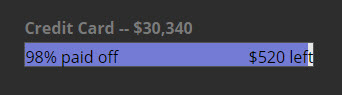

Meanwhile, back at the BatCave, I have some good news on the debt front. As you can see from my progress bars in the footer of this blog, I have made great progress on my credit card debt. I just received a year-end bonus at work. Yeah, I know it’s February, but that’s how my employer works. Anyway, I took every penny of it…well, every penny of what was left after taxes (ouch!), and put it towards the credit card debt.

I now have $520 left in credit card debt!. *screams*

It’s only a matter of days now before the final blade lowers.

I…CAN’T…WAIT..!!!!!

I can’t wait until I can finally end this credit card debt once and for all. I already have a nice place picked out for it to rest…eternally.

I get giddy with excitement every time I think about it. No more credit card debt. Gone forever and hopefully burning in the fires of hell where it belongs. Does this make me sound evil?

I assure all of you that I am not…well, not much. 😉 It’s just that $30,000+ of credit card debt has been financially strangling me for years. I have likely single-handedly financed someone else’s retirement with all the interest I’ve paid over the years. I will not be sad to see that debt die. 😈

Finally, I’ll be able to save up for a small savings fund. The next few months will give me a breather to save at least a $5k – $6k buffer, so I can sleep better at night. After that, I plunge into tackling my mountain of student loan debt. Watch out Sallie Mae, you’re next!

In another bit of good news, my retirement savings (investments) are accumulating faster than expected. I have increased my 2015 investment savings goal (including employer match) from a $20,000 total to an even more ambitious $30,000 total.

In the meantime, will DoubleDebtSingleWoman defeat the Evil Plastic Menace? Come back to see part 2. Same Bat time. Same Bat channel.

![]()

“Debtor’s prison is real, and opportunity cost is a bitch.” (DDSW)