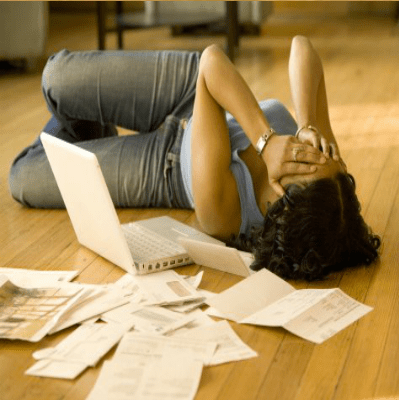

For too many of us, this is how we feel when trying to tackle our finances. I am a single woman with double debt. If you are reading this blog, you are likely a single woman (or man) with double debt. If not, consider yourself lucky. High debt loads are stressful enough for many couples to tackle together. Imagine shouldering six figures of debt on your own. For many of us, student loan debt is the biggest component of debt totals this high, but regardless of what got you here, you’re here now. And you have company.

.

Image credit:fallendeath13.deviantart.com

It’s that time of year. Just when you think your wounds are healing from spending another holiday season and New Year’s eve single and lonely – Valentine’s Day rolls around and it’s chocolate and rose-less passing reminds you that you are getting another year older – alone. Although being a single woman can be a great time of freedom, it can be depressing too. For those of us experiencing moderate to extreme debt burdens, facing it alone can be an additional challenge. What follows are some of the issues that we single women with deep debt have to face.

We have no partner to offer emotional or financial support

I am firm in the fact that I got myself into debt alone, so I will get myself out of it alone. However, having someone to keep me motivated, feels worth its weight in gold sometimes. Too many of us keep the extent of our debt secret out of shame, causing us to bottle up our fears and frustrations.

Most get out of debt articles and blogs with substantial debt payoff are about couples working together to make it happen. Their accomplishments are great, but I cannot relate to those stories. Having two incomes to tackle debt and sharing expenses is a luxury that we singletons don’t have. Being single can keep us in debt longer, and being in debt can keep us single longer. Fun huh?

And let’s not forget that women can stay trapped in stressful, abusive jobs because they have little or no safety net in the form of a partner to support them.

.

Pay inequality means that debt bites us harder and longer

Repayment affects us more because on average we earn less than men for the same work. Paying off the same debt burden as a man takes more money out of each of our paychecks and/or for a longer period of time. The gap may be shrinking, but there is still a ways to go.

.

The ticking biological clock or expense of raising kids adds pressure

Ladies, those of us in our 30’s and up are dancing the debt payoff two-step to a to a ticking biological clock. Forty-three percent (43%) of Generation X women don’t have children. Debt has been one factor in that. What if you are six figures in debt and pushing 40? By the time you pay off all your debt you’ll be peri-menopausal in your mid-forties at the earliest. Are you really expected to wait that long? Should you freeze your eggs and use surrogates? Some women with deep debt make the painful decision to never have children. Others become proponents of being child-free. If having children is extremely important to you, then have them; but be prepared for the financial effects and sacrifices that you’ll have to make.

If you already have children, you are more likely than men are to be their primary caregiver. Raising children today is more expensive than ever. Without a partner, even accounting for child support, women disproportionately shoulder the financial responsibility of child rearing, thus slowing down debt repayment.

.

Dating with debt is more difficult

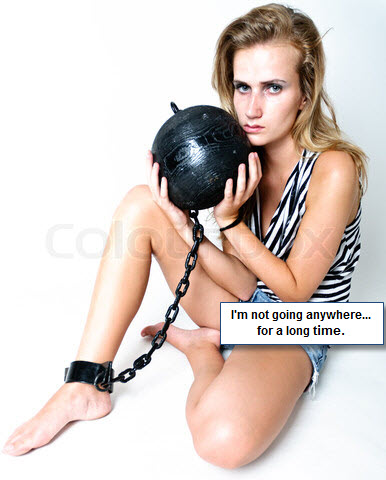

Research shows that women shackled with debt are less likely to marry. It doesn’t matter how sexy you are, debt is not attractive. Wait, what was I thinking. Of course how sexy you are matters. If you’re a Beyonce or Megan Fox clone, nothing on this list applies to you. For the rest of us, unfortunately, especially those of us dragging around a $100k+ ball and chain of debt and misery; we don’t look like a rockin’ good time to potential partners. We aren’t going to be on vacation with them running on an exotic beach anytime soon.

We often ask ourselves, ‘Am I undateable? Am I unmarriageble? Do I need to to pay off all my debt before pursuing relationships?’ As long as you are taking action to pay the debt off aggressively (not just talking about taking action), the answer to those questions is a resounding “No”. The same goes for anyone you may be interested in dating.

For all of us single ladies without a ring on it, debt does affect our romantic lives. If you can’t afford to travel or get involved with activities, it limits the pool of potential partners that you’ll have the opportunity to meet (online dating nothwithstanding).

Words of warning to my fellow single sisters in debt. Don’t let romantic partners use money as a way to control you. It’s not worth it. Don’t get into relationships for money. As a wise man Dr. Phil says, if you marry for money, you’ll earn every penny of it.

And, hey, if you can’t trust Dr. Phil, who can you trust?

.

Debt can damage our independence and self-actualization

Deep debt can change the dynamics of your relationships with other people. If enduring disdainful condescension or looks of pity aren’t bad enough, others may try to treat you like you are less than or helpless. You can’t afford to do the things that your friends and family can, and you may feel that your nose is being rubbed in it.

And if you are single woman and in deep debt, family, especially your parents, may have the view that because you don’t have a man/partner in your life to support you, that you still need their control help. Really? How many of us enjoy those conversations? Ladies, if this is the case, it’s time to start setting some boundaries.

Being a single woman is not easy. We all know that time is money, and commonly our time is not respected. Family volunteer you for things or pressure you into visiting far more often than you can afford to with respect to time and money. For some of us, the only trips we’ve taken in recent years have been guilt trips (bought and paid for by parents/family). First class.

Like potential romantic partners, some family members with ulterior motives may use money to try to control you and incur a sense of obligation on your part. Again, this is not worth it. Even if you repay the money, you may never be able repay the emotional debt (of their ‘saving you’) as far as the other person is concerned, which they will use to control you. Be very wary of taking monetary “gifts” from anyone that you don’t trust 100%. And of course, avoid taking loans from friends or family unless you want to ruin that relationship.

.

Harassment by debt collectors takes an emotional toll

We’ve seen the lawsuits and new stories. Women seem to be the targets of unduly nasty debt collector practices. Bullying, intimidation, and threats of sexual violence have driven some debtors to suicide, or the courtroom. Unfortunately, most women suffer in quiet anger, not knowing their rights or to whom to turn.

.

That is just some of what we deal with. Did I miss any? Are you experiencing any of these? Let me know in the comments.

.

“Debtor’s prison is real, and opportunity cost is a bitch.” (DDSW)