Happy New Year!

It is that time of year again. I unveil my 2015 financial goals. Before I do, I’ll look back at my recent yearly goals.

2014 Goals:

- Pay off remaining $22,770 balance in credit card debt

- Open and contribute to 401k up to point of employer match when eligible

2014 Outcome: [partial success]

- Paid off $16,780 in credit card debt [remaining balance: -$5,990]

- Paid $8,720 in student loan interest [0.o -Yeah, this is insane.]

- Opened and contributed to retirement funds [+$6,578 (including employer match)]

In the footer and sidebar, I have added a tracker for my retirement and other savings to help me have a fuller picture of my finances.

2015 Goals:

- Pay off remaining credit card debt of $5,990

- Reach $20,000 in retirement savings

- Reduce student loan debt to $108,000

- Save $6,000 in savings (Yes, my lack of an emergency fund is scary.)

- Pay cash for an international trip – $??

My student loan goal doesn’t look like much of a drop, but you have to remember that the first $750 that I pay each month is just going to interest, not principal. So it will take nearly $15k in payments to get from $113k to $108k.

Undoubtedly, I have some more thinking to do to figure out how to prioritize all of these goals. Save for retirement or pay down debt?

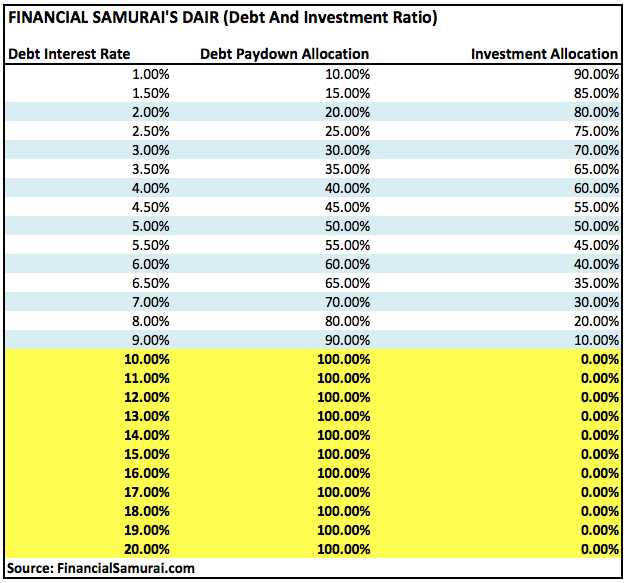

Will a noble samurai rescue me from my quandry? Enter FS-DAIR

Financial Samurai has posted a formula for determining how to prioritize debt repayment vs. retirement funding. His FS-DAIR (Financial Samurai Debt and Investment Ratio), looks like the tool I’ve been hoping to find for a while now. How does it work? This chart lays it all out in a clear format.

Source and Image Credit: FinancialSamurai.com

Basically, any debt that you have carrying 10% or higher in interest, should be paid off post-haste, at the expense of any investing (beyond the 401k employer match). Once your debts have interest rates at 9% and below, things get interesting. Read Sam’s FS-DAIR post for examples of how this works. For instance, Sam uses the following as an example for someone deciding how much to put toward student loans vs 401k.

Source: FinancialSamurai.com

My student loan debt is made up of many separate loans with different fixed interest rates. I will need to run the numbers to see how this would shape my plan of attack. I’ll do a follow-up post on this in the not too distant future. Thanks, Sam for lending me a sword to use in my battle!

Net Worth – Double Debt Single Woman – January 2015

As my debt drops in 2015, I’ll be tracking my Net Worth. My first goal will be to see it drop down into the 5-digit zone. Soon you will also be able to track it here @Rockstar Finance. I will be pretty low on the ranked list, but I will be gunning for higher and higher slots. Watch out Finance Phoenix and Feisty Finance!

“Debtor’s prison is real, and opportunity cost is a bitch.” (DDSW)

I’m really glad you’ve started a retirement account alongside everything else. The FS chart is really interesting and I wish I’d seen it a couple of years ago; I decided to concentrate on paying down loans before I invested anything but in retrospect I think this was a mistake. If I were doing it all over again…well, if I were doing it all over again I wouldn’t have taken out loans 🙂 But my debt was split between 5.5% and 6.5% loans and I think I should have started *some* kind of retirement account a year earlier than I did. Probably it won’t end up making an enormous difference thirty years from now, but still, on principle, I think people our age should be setting something aside.

I had $75 in my emergency fund until late summer. I had to laugh every time I looked at it because it was better than crying in fear 🙂

Do you use Ready for Zero or some other kind of tool to keep track of all the loans? I only had two, plus the credit cards, so they weren’t that hard to manage, but I’m always amazed at how people who have ten or twelve smaller loans keep from accidentally defaulting.

LikeLike

Yeah, hindsight is 20/20 vision. If I could go back 20 years, I would have made a lot, A LOT of different choices. Sigh…

Agreed!

I do have a Ready for Zero account which shows all of my individual loans and recommends which ones to attack in order of interest rate and debt size. So I will also use that as a guide. Thanks for the heads up.

LikeLike

I really think you should read Total Money Makeover. It will really make you think differently about your priorities. Good luck!

LikeLike

Nice work on yours strides towards your 2014 goals… and Setting new goals for the year ahead in 2015!!! Looks like you have been killing it the past couple of years… AWESOME JOB!!! Networth is a great tracker to look at your overall position.

LikeLike